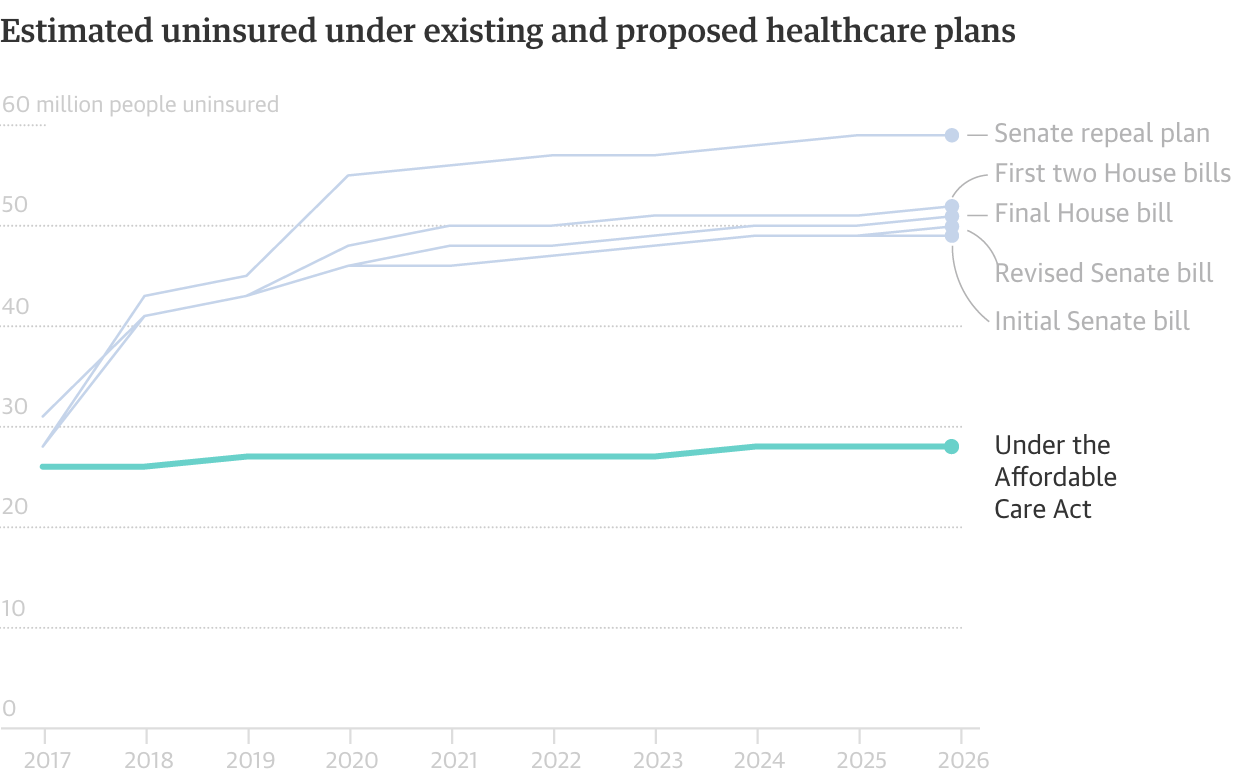

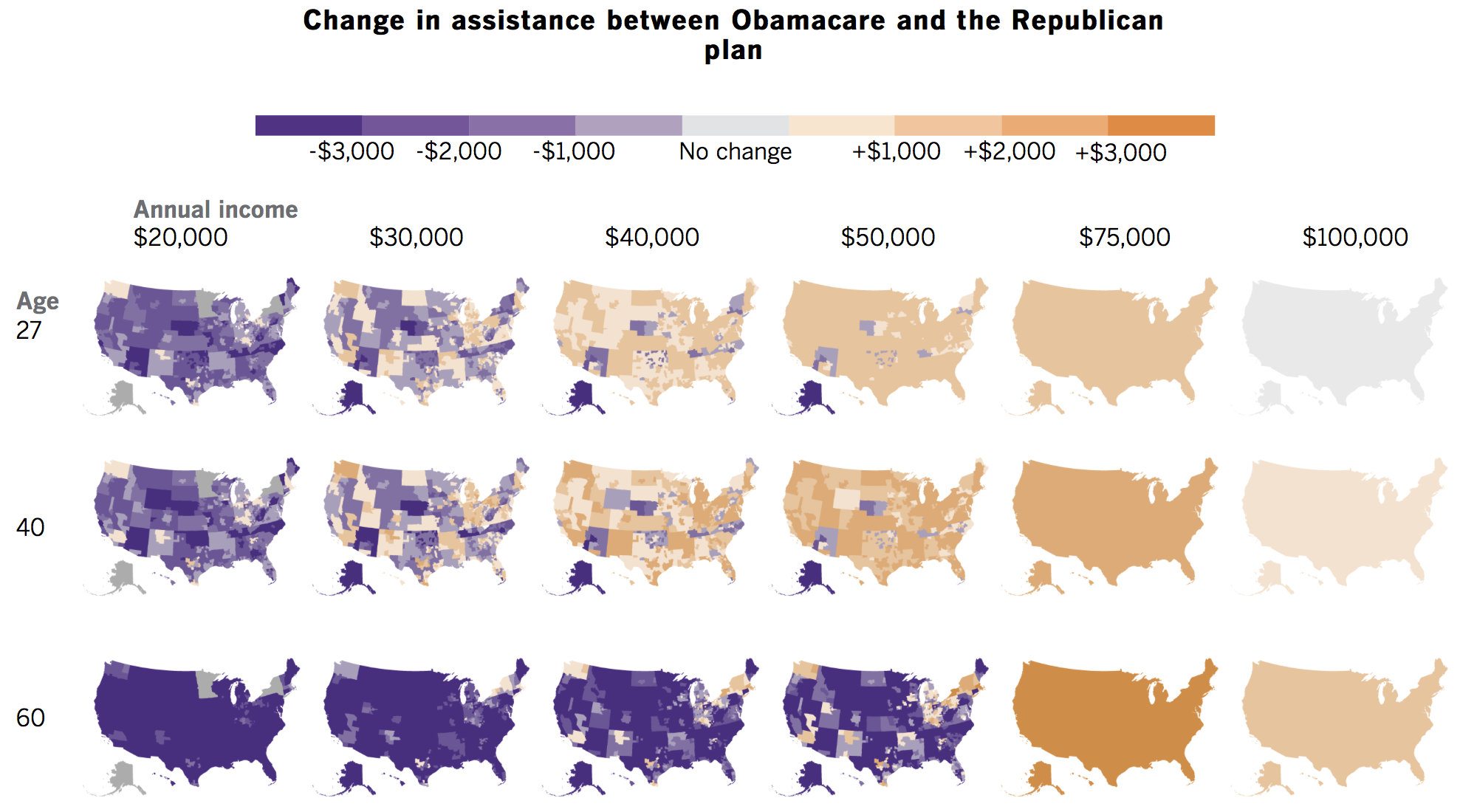

While I am still looking for a graphic about Zimbabwe, I also want to cover the tax reform plans as they are being discussed visually. But then the Senate went and threw a spanner into the works by incorporating a repeal of Obamacare’s individual mandate. “What is that?”, some of you may ask, especially those not from the States. It is the requirement that everyone have health insurance and it comes with tax penalties if you fail to have coverage.

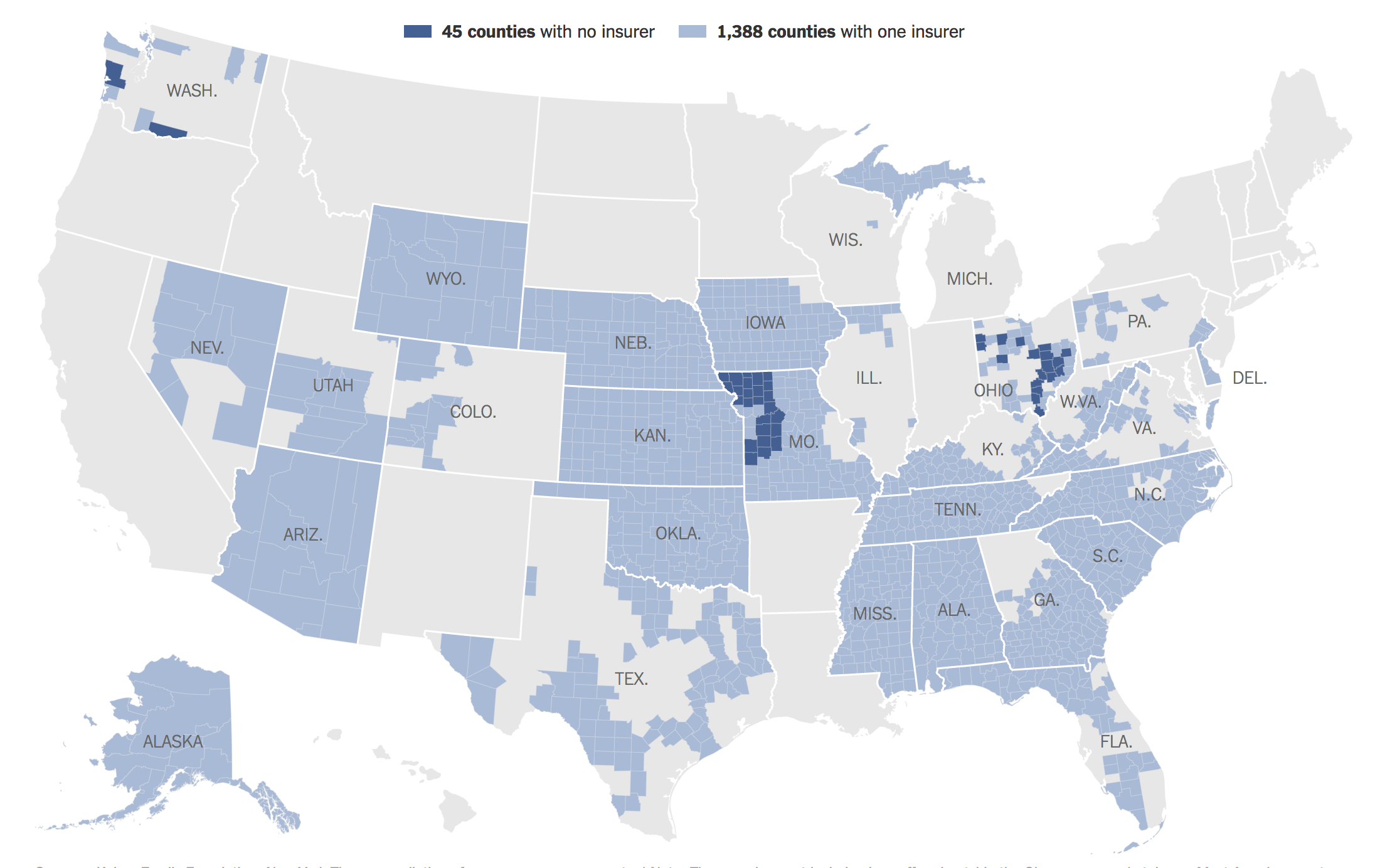

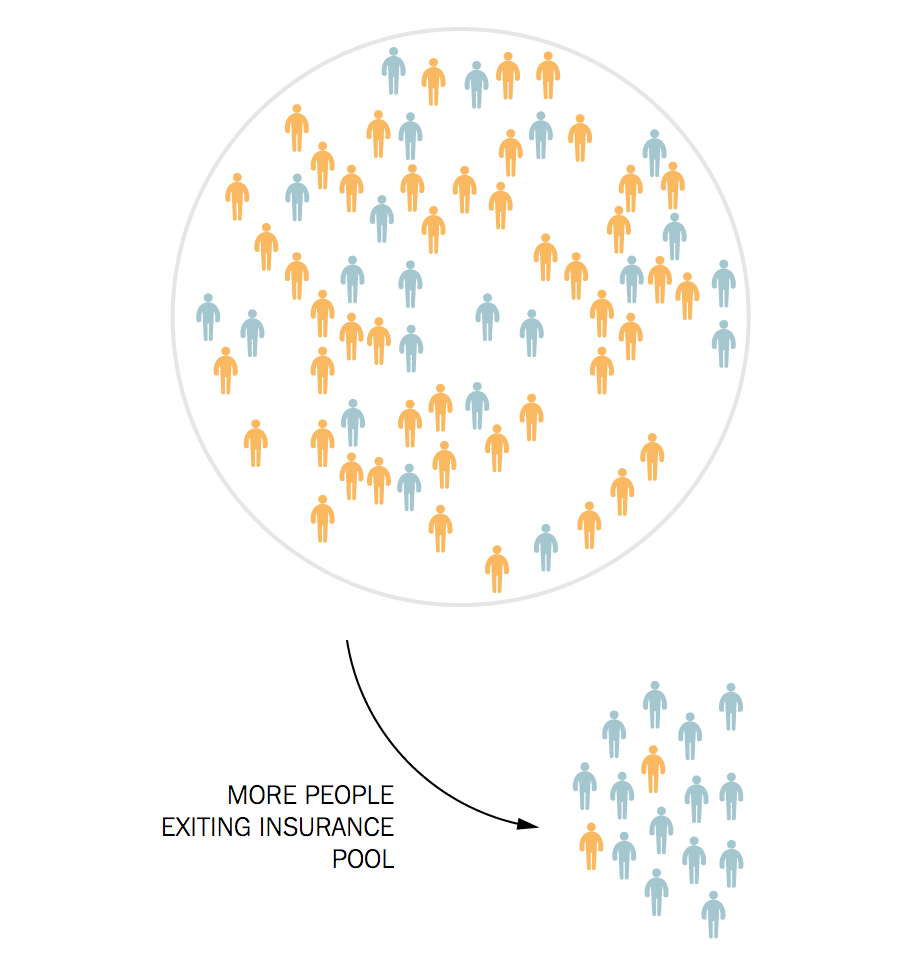

Thankfully the New York Times put together a piece explaining how the mandate is needed to keep premiums low. Consequently, removing it will actually only increase the premiums paid by the poor, sick, and elderly. The piece does this through illustrations accompanying the text.

Overall the piece does a nice job of pairing graphics and text to explain just why the mandate, so reviled by some quarters, is so essential to the overall system.

Credit for the piece goes to Haeyoun Park.